1) Create and Stick to a Budget

Budgeting is one of the simplest yet most foundational elements of financial planning. A clear understanding of where your money goes gives you the power to control your spending and savings, making it easier to achieve your financial goals. By budgeting, you can also improve your credit score and avoid running monthly deficits or relying on credit cards for unexpected expenses.

Types of Budgets

Here are five different types of budgets to consider:

- The No-Budget Budget

This is a flexible spending plan that takes two main factors into account:

- Net pay for the month

- Your “must-pay” expenses for the month

This budget works best when your needs are low enough that you don’t require additional funds for basic expenses. Once you’ve covered all your necessary costs (e.g., rent, bills, car payments, insurance), the remaining money becomes disposable income. There’s no need to track every expense as long as you stay within your limits and avoid overdrawing your bank account.

While this approach is simple, it can be challenging for some to differentiate between their wants

- Pay-Yourself-First Budget

Also known as “reverse budgeting,” this method prioritizes savings and investment goals. With this approach, you set aside money for your savings and investment accounts before addressing other expenses.

The main objective is to meet your financial goals, with everything else coming second. After funding your savings and investments, you allocate funds for recurring expenses like rent/mortgage, utilities, car payments, and student loans. Any remaining money can be used for discretionary spending or “fun money.”

This budgeting method works well for individuals without significant monthly credit card balances, as it can otherwise be difficult to track available funds. It’s also ideal for those who prefer a straightforward approach and are committed to achieving their financial goals in a timely manner.

- Envelope System

The envelope system is a traditional, cash-based budgeting method. Although it might seem outdated in 2025, modern budgeting apps now offer digital equivalents like “buckets” or “vaults” for allocating funds.

Here’s how it works: You determine how much money you need for specific categories (e.g., rent, groceries) and allocate cash to labeled envelopes for each category. Once an envelope is empty, you’re not allowed to spend more on that category unless you move money from another envelope.

This method is excellent for those who want strict control over their spending, especially if they struggle with credit card debt. However, frequently moving money between envelopes can undermine the budget’s effectiveness, particularly for essential expenses.

- Zero-Based Budget

A zero-based budget is similar to the envelope system but offers greater flexibility and doesn’t rely solely on cash. In this approach, every dollar of your income is assigned a specific purpose. At the end of the month, your total income should equal your total expenses.

This method requires detailed planning and tracking of multiple categories, including savings, bills, and discretionary spending. If you don’t use all the money allocated for a specific category (e.g., fun money), you’ll already have a plan for reallocating those funds.

The zero-based budget is ideal for individuals who want precise control over their finances and are comfortable managing their money at a granular level.

- 50/30/20 Budget

One of the most popular budgeting methods, the 50/30/20 rule divides your income into three categories: Needs, Wants, and Savings/Investments.

- 50% for Needs: This includes non-negotiable expenses like housing, bills, groceries, and gas. If your needs exceed 50% of your income, you may need to reduce luxury expenses to stay within this limit.

- 30% for Wants: This category is for discretionary spending, such as entertainment, dining out, or shopping. These are things you want but don’t necessarily need.

- 20% for Savings/Investments: This portion goes toward achieving your savings and investment goals. For example, if you’re saving for a house, you may prioritize savings over investments. Conversely, if you’re focused on retirement and already own a home, you might invest more aggressively.

This method is straightforward and helps you identify areas where you may need to cut back to achieve a balanced budget.

2) Build an Emergency Fund

Building an emergency fund is essential if you want to avoid being overwhelmed by unexpected expenses. The primary purpose of an emergency fund is to minimize the financial impact of emergencies.

We’ve all heard stories about families who were set back for years due to disasters like floods or house fires. Often, these situations arise because the family wasn’t able to keep up with necessary maintenance. For example, neglecting routine upkeep can lead to a flooded basement requiring expensive repairs. Without an emergency fund, this type of situation can force a family to rely on credit cards or loans, incurring interest and further financial strain.

The importance of having an emergency fund cannot be overstated. It protects you from having to make costly financial decisions during times of crisis. Instead of accumulating debt, you can draw from your emergency fund to handle these unexpected expenses.

As of August 2023, here is a list of estimated costs for full replacement of common home repairs:

- Roof: $5,700–$16,000

- Foundation: $4,600–$19,400

- Water Heater: $800–$3,500

- HVAC System: $7,000–$16,000

- Septic System: $3,000–$15,000

While some of these costs might seem manageable, they can still cause significant inconvenience. For instance, imagine not having a functioning HVAC system on a hot and humid August day—what is the cost of that discomfort? The higher-end figures can be particularly daunting, underscoring the importance of securing your emergency fund.

A good rule of thumb is to budget about 1% of your home’s value annually for repairs. However, this doesn’t account for other potential emergencies, such as medical bills, car repairs, or other unexpected costs. By building a robust emergency fund, you can safeguard your financial stability and handle unforeseen expenses with confidence.

3) Pay Down High-Interest Debt

Paying off high-interest debt is one of the most effective strategies to relieve the burden of monthly minimum payments and escape the cycle of debt. In today’s economic climate, credit card debt continues to rise year after year with no signs of slowing.

According to WalletHub, as of September 9, 2024, the average individual owes $6,501 in credit card debt, while the average household owes over $10,000. Forbes reports that the average annual percentage rate (APR) for this debt is a staggering 28.75%. Such high rates can cripple families, making it even harder to climb out of debt.

The rising prevalence of credit card debt has left many struggling to keep up with minimum payments, resulting in a vicious cycle of using high-APR credit cards to cover everyday expenses. High-interest debt—whether from credit cards, student loans, or car loans—is a significant barrier to financial freedom. These debts force families to prioritize payments, and during financial hardship, they often face difficult decisions about which loans to let go delinquent.

The relationship between economic conditions and loan delinquencies is clear. During periods of rapid inflation or recession, there’s a noticeable increase in borrowers falling behind on auto loan payments. This trend is often driven by factors such as:

- Job loss

- Reduced wages

- Lifestyle inflation

- Inflationary pressures caused by government stimulus measures

Inflation increases the cost of goods and services, straining household budgets and making it harder to stay current on loan payments.

Paying down high-interest debt can have long-term benefits. It not only reduces financial stress but also frees up cash flow that can be redirected toward more productive uses, such as investing in retirement or building an emergency fund. By focusing on eliminating high-interest debt, you can break free from the cycle of debt and create a more stable financial future.

4) Saving for Retirement

Saving for retirement is often procrastinated until individuals reach their 30s, but starting early makes a significant difference. The earlier you begin, the more you can benefit from the power of compound growth. Developing the discipline to consistently save for retirement is an essential part of building a strong financial profile.

The importance of starting early becomes clear when comparing the growth potential of investments made at different ages. Consider the following example using the future value formula:

FV = PV × (1 + r)^t

Where:

- FV = future value

- PV = present value (initial investment, $1 in this case)

- r = annual rate of return (assumed to be 7%)

- t = time (number of years)

For a 20-year-old investing until age 65, the growth multiple of a single dollar is approximately 21x. In contrast, for a 30-year-old investing for the same return until age 65, the growth multiple is only 10.68x.

This means that every dollar invested by the 20-year-old grows to 21 times its initial value, while the same dollar invested by the 30-year-old grows to just 10.68 times its value. This stark difference highlights the importance of starting early, as the power of compounding diminishes slightly with each passing year.

If you’re unsure where to begin saving for retirement, explore the options available to you:

- Employer-Sponsored Plans: Does your employer offer a 401(k) with a match? Take advantage of this free money.

- Individual Retirement Accounts (IRAs): Look into Traditional IRAs and Roth IRAs to see which suits your financial situation and tax strategy.

Don’t Overlook Insurance

Another critical, often overlooked, aspect of retirement planning is insurance. If you’re part of a dual-income household, ensuring that you and your spouse have adequate life insurance is crucial. The loss of one income due to premature death can severely impact your family’s living situation and jeopardize long-term financial goals, including retirement.

Without proper insurance coverage, the surviving spouse may need to stop retirement contributions to maintain the family’s lifestyle, leading to a shortfall in retirement funds when the time comes.

Take Action Today

Saving for retirement is one of the most impactful financial decisions you can make. Start early, invest consistently, and review your options to maximize your retirement savings.

5) Set SMART Financial Goals

Setting SMART goals provides a clear and effective framework for achieving financial success. By ensuring your goals are Specific, Measurable, Achievable, Relevant, and Time-bound, you can create a plan that aligns with your unique circumstances. This structured approach fosters clarity and accountability, making it easier to stay on track and achieve your financial objectives.

Here’s a breakdown of the SMART acronym and what each component involves:

S: Specific

Your goal should be well-defined and precise. Avoid vague statements; instead, clearly outline what you want to achieve. Ask yourself:

- What do I want to accomplish?

- Why is this goal important to me?

- Who will be involved?

- Where will this take place (if applicable)?

For example: “Save $5,000 for a family vacation to Hawaii by December 2025” is more specific than “Save money for a vacation.”

M: Measurable

A measurable goal allows you to track your progress and stay motivated. Quantify your goal so you can evaluate success.

- How much?

- How many?

- How will I know when it’s accomplished?

For instance: “Save $500 per month for 10 months” provides a clear measurement compared to “Save money consistently.”

A: Achievable

Your goal should be realistic and attainable within your current circumstances. Ambitious goals are great, but they should also be grounded in practicality.

For example: If you’re buried under student loans, credit card debt, and a car loan, it’s unrealistic to aim to pay off your mortgage in a single year. Instead, break it into smaller, actionable steps, like paying off credit card debt within a year before tackling larger debts.

R: Relevant

Relevance ensures your goal aligns with your broader financial priorities and personal circumstances. Irrelevant goals can quickly lose significance and derail your motivation.

Ask yourself:

- Does this goal matter to me?

- How does this goal fit into my broader financial plan?

- Is it the right time for this goal?

For example: Paying off debt may be more relevant than saving for a luxury purchase if you’re struggling to meet monthly expenses.

T: Time-Bound

Setting a clear deadline creates a sense of urgency and helps you stay focused. Break down long-term goals into smaller milestones with specific time frames.

For instance: Instead of saying, “I want to pay off my debt in 20 years,” refine the timeline. Start by targeting specific debts:

- Pay off credit card debt within 1 year.

- Eliminate personal loans in 2 years.

- Pay off the car loan in 3 years.

- Focus on the mortgage last, within the remaining timeline.

Time management adds structure and ensures you remain accountable to your financial goals.

By setting SMART financial goals, you can create a roadmap tailored to your needs and aspirations. This method helps keep your objectives clear, actionable, and relevant, increasing the likelihood of achieving lasting financial success.

Cut Unnecessary Subscriptions

Subscriptions can make our lives easier and more convenient, but they also have a sneaky downside—they’re easy to forget about. Left unchecked, subscription expenses can pile up unnoticed, especially since they tend to increase in price over time rather than decrease.

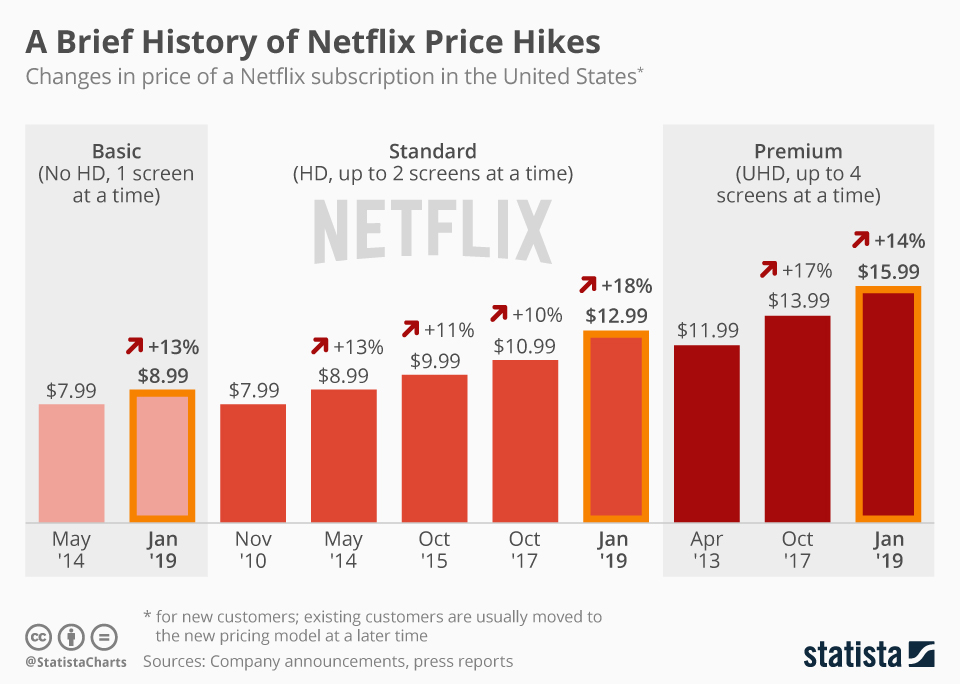

Consider the example of Netflix:

In 2019, Netflix’s premium tier was already climbing in price, and as of 2024, the cost has reached $22.99 per month. This trend isn’t unique to Netflix. Many other popular subscriptions have seen similar price hikes:

- Hulu (Ad-Free Plan): Started at $12/month in 2015; now $18.99/month, with optional add-ons:

- Max (With Ads): $9.99/month

- Max (No Ads): $16.99/month

- Paramount+ with SHOWTIME: $12.99/month

- STARZ: $10.99/month

- Amazon Prime Video: Previously included ad-free streaming with the standard Prime membership. By 2024, ad-free streaming now costs an extra $11.99/month.

- YouTube TV: Increased from $64.99/month in 2023 to $72.99/month in 2024. As of December 2024, YouTube has announced another price increase for 2025, raising it to $82.99/month. Adding the NFL Sunday Ticket for out-of-market games costs an additional $479 per season.

| Year | Price (Per Month) | Notes |

| 2017 | $35 | Initial launch price |

| 2018 | $40 | Price increased after adding more channels |

| 2019 | $50 | Further channel expansion |

| 2020 | $64.99 | Added Viacom, CBS channels |

| March 2023 | $72.99 | First price hike in three years |

| December,2024 | $82.99 | Effective for new subscribers immediately, for existing users in Jan 2025 |

When you break it down, it’s easy to see how these subscriptions can quickly add up, draining your wallet for minimal added value. Ask yourself: How many streaming services does your household really need to stay entertained? Where can you cut back?

Subscriptions Beyond Entertainment

While streaming services are often the first to come to mind, it’s important to recognize that subscriptions encompass more than just entertainment. Other recurring expenses can include:

- Cell Phone Providers: Are you paying for features or data you don’t use?

- Internet Providers: Have you shopped around for better rates recently?

- Landscaping Services: Could you do the work yourself instead of outsourcing?

- Insurance Policies: Can you switch providers to get the same coverage at a lower cost?

Reallocating Savings

By identifying and cutting unnecessary subscriptions, you can free up more cash flow toward your financial goals:

- Invest more aggressively

- Save for a down payment on a home

- Spend on meaningful experiences or gifts

- Build an emergency fund

Every dollar saved from unnecessary subscriptions is a dollar that can be redirected to create long-term value. With a little effort and discipline, you’ll find yourself with more financial flexibility and less waste.

7) Automate Your Finances

Automating your finances is a simple yet effective way to take control of your money without constantly having to think about it. Financial automation allows you to set up regular transactions on a schedule, so things get done without you having to manually manage them.

By automating tasks such as paying bills, transferring savings, or making investment contributions, you eliminate the need to remember every detail and ensure things happen on time. This helps you avoid late fees and missed payments while making sure you’re consistently saving and investing.

Automation can stretch your dollars further by taking the pressure off your shoulders. Once everything is set up, you don’t have to manually decide where every single dollar goes or move money around. Instead, your money works for you automatically, making the process of managing finances simpler and more efficient.

8) Create a Debt Payoff Plan

Half of the battle when it comes to achieving financial goals is creating a plan to reach them. In the case of paying off debt, there are two of the most effective methods: Debt Snowball and Debt Avalanche.

Debt Snowball:

The Debt Snowball method focuses on paying off the smallest debt first, regardless of its interest rate. Once the smallest debt is paid off, you move on to the next smallest, and so on until all debts are eliminated.

But doesn’t this method result in paying more interest over time? Yes, it does! However, the Debt Snowball method isn’t designed for maximum interest savings, it’s designed for motivation. By paying off smaller debts first, you gain quick psychological wins, which can boost your confidence and keep you motivated to tackle larger debts. This method is ideal for someone who needs that sense of accomplishment to stay committed to their debt repayment journey.

Debt Avalanche:

The Debt Avalanche method works by prioritizing the debts with the highest interest rates first, while making minimum payments on the others. Once the highest-interest debt is paid off, you move on to the next one.

This method saves you money in the long run by reducing the amount of interest paid, but it may lack the immediate “wins” that come with the Debt Snowball approach. The Debt Avalanche method is best for someone who is focused on minimizing the overall cost of their debt and can stay motivated without the psychological boosts that come from paying off smaller debts first.

Which Method is Best?

Both methods are effective, but the choice depends on your personal preferences and motivation style. If you thrive on quick wins, the Debt Snowball method may be a better fit. If you are more focused on minimizing interest costs and can stay disciplined without immediate rewards, the Debt Avalanche method may work better for you.

Regardless of the method you choose, both require consistent budgeting, discipline, and determination to succeed.

9) Start investing

Investing is one of those things that often gets pushed off until it “feels right” but in reality, the earlier you begin to invest, the more you will have when its time to pull from those investments. We have already touched on the idea of compound growth and the time value of money so you should already know that a dollar invested today is going to be worth a whole heck of a lot more in 40 years vs if you kept that same dollar, not invested it would get its value ate away by the invincible killer of inflation. Investing allows your money to keep up and even outpace the inflation rate, it increases the pricing power of your dollars when done the right way. Your investment dollars don’t need to be used for retirement only, they can be used to purchase the dream home, or make a large investment into something else, make donations do your favorite foundations, or set your kids up for life. The whole point here is that getting the individual to actually begin investing is the hardest part of the plan, people often overcomplicate finding the right brokerage account, they want to do all the research in the world on different accounts, mutual funds, ETF’s, etc. people often are drawn to the idea of day trading, when in reality the best way to invest is to have time in the market, not timing the market.

10) Improve Your Credit Score

A good credit score is incredibly useful—it allows you to secure favorable rates on large purchases like homes, investment properties, vehicles, loans, and more. Without a good score, you may not get access to these opportunities or may face higher rates on loans. If your score is on the border between good and bad, you may miss out on the best rates.

How is Your Credit Score Calculated?

Your credit score is determined by five key factors, each weighted differently:

- Payment History (35%)

- Amount Owed (30%)

- Length of Credit History (15%)

- New Credit (10%)

- Credit Mix (10%)

Payment History (35%)

This factor tracks your payment behavior across all your credit accounts, dating back to when you first started using credit. It considers how often you pay on time, whether you’ve missed any payments, or if you’ve paid late. The more consistently you make on-time payments, the better your score. Missed or late payments will negatively impact it.

Amount Owed (30%)

This factor compares your total credit limit across all accounts to how much you owe. For example, if you have a $1,000 limit on a credit card and owe $500, your ratio is 50%. It’s generally recommended to keep your credit usage below 30% for optimal scoring. Ideally, you should pay off your credit cards in full every month to avoid interest and fees.

Length of Credit History (15%)

Your credit history length is one factor you can’t speed up—it takes time. The longer you’ve been using credit responsibly, the better. One way to help build a young person’s credit history is by adding them as an authorized user on your credit card. This way, they can start building a credit history early.

New Credit (10%)

New credit refers to how many new credit accounts you’ve opened within the past year. Opening several accounts in a short time can make you look like a riskier borrower, especially if you plan to apply for a larger loan like a mortgage. It’s fine to open a new account every year or so, but avoid opening multiple accounts right before applying for a big loan.

Credit Mix (10%)

Credit mix refers to the different types of credit you have, such as credit cards, car loans, or mortgages. Lenders look for a balanced credit mix, which indicates that you’re able to manage different types of credit responsibly. A healthy mix can improve your score, but it’s more important to focus on responsible use rather than simply opening new accounts to diversify your mix.

Improving Your Credit Score

Improving your credit score requires a combination of efforts in all aspects of your finances. You need to be disciplined about avoiding maxing out your credit cards, making payments on time, keeping your credit utilization low, and not opening too many new accounts at once. While it may take time and effort, the payoff of a higher credit score is worth it. A good credit score can make your financial life significantly easier by securing better rates and more opportunities.

Advisory Services offered through Nepsis, Inc., An SEC Registered Investment Advisor.

Sources

New Year, New You: Top 15 Financial Resolutions For 2025

Average Credit Card Debt in 2024 & Historical Balances

What Is The Average Credit Card Interest Rate This Week? – Forbes Advisor

Auto Loan Delinquencies Hit 13-Year High As Monthly Car Payments Get Bigger

401k Calculator: Estimate your Future Balance – NerdWallet

Chart: A Brief History of Netflix Price Hikes | Statista

{kind=link}

How Is My Credit Score Calculated?

What Are the Average Costs of Common Home Repairs?

Subscription cost of U.S. video streaming offers 2024 | Statista

YouTube TV price increase: How much more you’ll spend | AP News